In vs. Out of Network: How do I decide?

Understanding how to use insurance to access mental/behavioral health benefits.

There are pros and cons to going in and out of network. Going “in network” means that you will be using your insurance benefits to pay the therapist directly for services. You may owe a copay, or your insurance may require you to pay the full amount until you hit a certain monetary amount. At that point, they will cover the amount of therapy. This is called “meeting your deductible”.

Going “out of network” means that your therapist does not accept your insurance benefits. Therefore, you would be paying your therapist directly. You can use your HSA or FSA benefits sometimes to cover this. IF you have insurance benefits, your insurance MAY cover your cost of therapy. It depends and you would need to contact them directly to get more info. Now that we have laid some framework, let’s delve into the pros and cons of using each.

In Network

PROS:

* most of the cost of your therapy will be covered

* it helps narrow down available therapists

* it helps you reach your insurance deductible

CONS:

* your insurance company may decline to pay for part of or all of your services and you are required to pay for whatever your insurance company does not cover

* your therapist may have to submit a psychiatric diagnosis, treatment plan, and progress reports to your insurance company to justify your services

* some people find this to be invasive

* if you have a high deductible and only need a few sessions, you may end up paying out of pocket anyways

Out of Network

PROS:

* your money is going directly to your therapist and is not providing profits for corporations

* your therapist is reimbursed at a fair rate (many insurance companies pay therapists a low/insufficient fee for each session) ensuring that your therapist does not have to overload their schedule or work overtime to pay bills… so your therapist is at less risk of burnout and is better able to help YOU!

* you can maintain confidentiality more easily, as there is no third party involved

* you may be able to use your HSA or FSA benefits to assist with payment

* your insurance company may reimburse you for services

CONS:

* if you submit your bills to insurance for reimbursement, your insurance company will require a psychiatric diagnosis from your therapist… this is something that may or may not benefit you

* it can be an expensive investment

IF you choose to go with an out of network provider, you may be able to have their services reimbursed by your insurance company. First, I recommend that you call your insurance company (number on the back of your card) and ask if they do reimburse for out of network providers. There may be a deductible you need to meet or some other stipulations that you should know of. It is also important to understand how your insurance company wants you to submit documentation to them. It may be via email or regular USPS mail.

If your insurance does accept super bills, it’s important to ask any potential therapist if they supply super bills. A super bill can be quickly made by having the therapist putt the following information on any invoice:

1. Your identifying information

2. Their practice information and tax ID number

3. Dates of service and service type

4. CPT code (your therapist can look this up online) for service

5. Your diagnosis

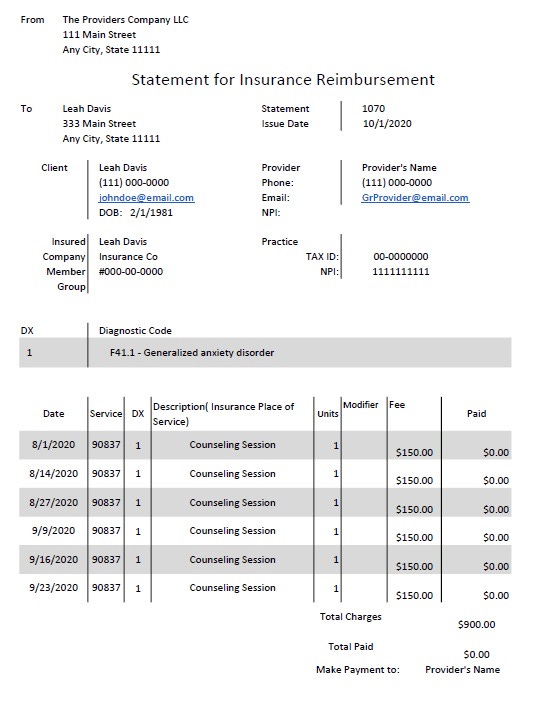

Below is an example of a superbill:

Make sure that your therapist is on board with creating this document for you. The therapist will send you this document and then you will be responsible for submitting it to your insurance company.

It may seem difficult, but in a few quick and easy steps you can easily make an out of network provider financially feasible for you!